Does the business have the capability to justify a premium valuation?

Future Revenue Creation Capacity™

Capability to create and capture future growth

Assessment Illustration

M&A Advisor Summary — 24-Month Monetisation Maturity & Valuation Expansion Outlook

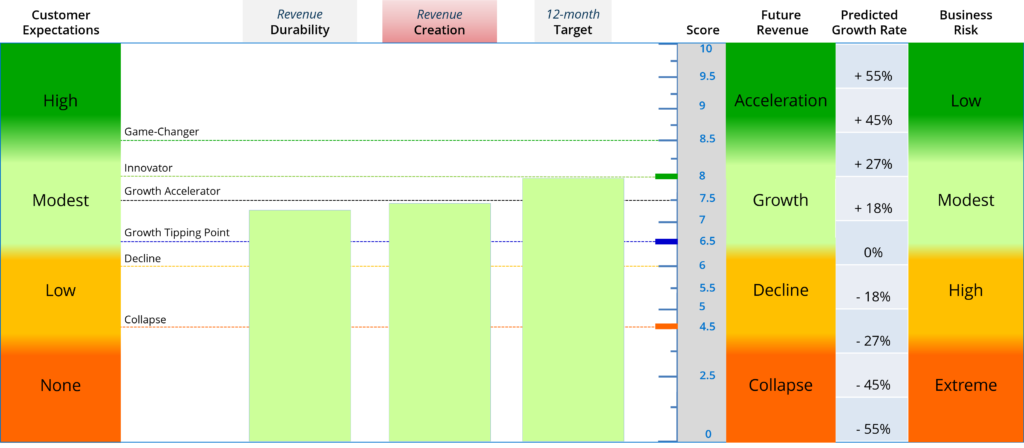

The company’s Future Revenue Creation Capacity score of 7.4, supported by strong Adapt (7.78) and Innovate (7.5) capabilities but constrained by lower Execution (6.7), positions it in the upper Growth Accelerator range, with a credible trajectory toward Innovator-level monetisation strength (8.0+) over the next 24 months. This indicates improving revenue quality and valuation expansion potential, with execution maturity as the primary determinant of deal attractiveness and post-transaction upside.

Post-Assessment Opportunities

The opportunities below were identified through the Future Revenue Creation Capacity assessment to strengthen the company’s ability to create new revenue. They complement the customer-validated Revenue Durability opportunities identified in the previous section, together providing a balanced view of the external opportunities and internal capabilities required for sustainable growth.

These opportunities have been incorporated into a company-wide Future Revenue Creation Roadmap, enabling teams across multiple functions to strengthen the three core growth capacities below. Each capability is measured and scored at the individual, team, and company levels, aligning every employee with customer opportunities and the company’s future revenue creation objectives.

Capacity to Adapt

- Improve visibility of emerging customer opportunities.

- Increase customers’ expectations of value and willingness to pay a premium.

- Build confidence to pursue ambitious growth opportunities.

- Strengthen motivation and commitment to achieve ambitious goals.

Capacity to Innovate

- Increase the ability to create unique customer value aligned with commercial objectives.

- Strengthen collaboration across teams.

- Build collective commitment to achieving financial outcomes.

- Increase focus on creating new customer value.

Capacity to Execute

- Improve the capability to execute ambitious goals consistently and with precision.

- Strengthen the organisational capacity to sustain long-term growth.

Following the assessment, the leadership team established a 12-month Future Revenue Creation Capacity Score™ target of 8.0 to achieve Innovator-level revenue creation capability.

M&A Decision Signals

1. Pricing Power

View: Improving, not yet fully embedded

Pricing power is supported by strong adaptability and innovation, suggesting the business can increasingly justify value-based pricing. However, inconsistent execution limits the consistency with which pricing strength is realised across customers and segments.

Opportunity: Gradual strengthening of pricing discipline and value capture post-transaction.

Risk: Pricing leakage or inconsistent monetisation if execution gaps persist.

2. Revenue Scalability

View: Strong structural scalability with execution drag

The company demonstrates high underlying scalability potential, driven by its ability to adapt and innovate in response to customer needs. However, execution constraints currently reduce the efficiency and consistency of scaling revenue.

Opportunity: Significant upside in scaling efficiency as execution matures.

Risk: Scaling inefficiencies may increase cost-to-serve or slow expansion velocity.

3. Margin Expansion Potential

View: Meaningful upside, execution-dependent

Margin expansion potential is present due to strong top-line drivers, but currently constrained by execution inefficiencies. As execution improves, the business should benefit from operating leverage and improved monetisation discipline.

Opportunity: Material EBITDA expansion potential over 24 months.

Risk: Delayed or limited margin improvement if execution remains inconsistent.

4. Execution Maturity

View: Primary constraint on valuation realisation

The Execution score of 6.7 is the weakest component of the model and sits just above the Growth Tipping Point threshold. While not structurally weak, it indicates that the organisation is not yet consistently converting innovation and adaptability into fully optimised revenue and margin outcomes.

Opportunity: Clear value creation lever through operational improvement and integration discipline.

Risk: Execution shortfalls could materially limit realisation of pricing, scalability, and margin upside.

Overall M&A Interpretation

The company presents a strong underlying monetisation profile with significant 24-month upside potential, currently constrained by execution maturity rather than demand or innovation capability. The trajectory toward Innovator-level monetisation strength (8.0+) suggests improving pricing power, scalable revenue generation, and meaningful margin expansion potential over time.

From an M&A advisory perspective, this is a business with clear valuation expansion potential post-improvement of execution discipline, where deal value is likely to be highly sensitive to the acquirer’s ability to enhance operational consistency and fully unlock embedded monetisation capacity.

Valuation Expansion Improvements

Ongoing performance improvements are achieved through the application of Growth Predictor’s platform to identify where revenue potential is not being fully realised, and where capability constraints or customer misalignment are limiting growth. This enables more focused strategic prioritisation and faster execution of improvement initiatives.

The platform applies the 16-stage Future Revenue Creation Roadmap to core workflows to surface, prioritise, and monetise opportunities, while improving overall organisational effectiveness in order to:

- adapt to evolving customer needs

- develop and shape innovative solutions to emerging problems

- execute new value propositions with greater speed and precision