Is the revenue base durable enough to justify valuation?

Revenue Durability™

Capability to win, retain, and expand customers

Assessment Illustration

M&A Advisor Summary — 12-Month Revenue Quality & Buyer Confidence Outlook

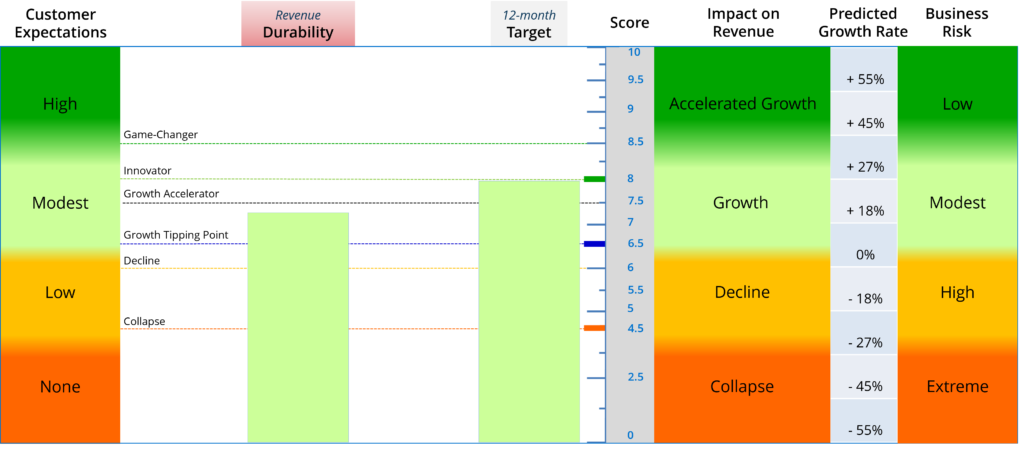

The company’s Customer & Revenue Strength score of 7.3, above the sector average of 7.0 and trending toward a 12-month target of 7.9, places it in the upper Growth Accelerator range. This indicates improving revenue quality and increasing customer-driven stability, with a clear trajectory toward stronger durability and higher buyer confidence over the next 12 months.

Post-Assessment Opportunities

The Revenue Durability Assessment™ uncovered the customer-validated opportunities below through structured conversations about the innovative value customers expect the company to deliver in the future. This customer rating process builds trust, measures how well the company is adapting to evolving customer expectations, and creates a platform for strategic discussions that uncover new revenue and growth opportunities.

Sales: Five immediate sales opportunities were identified, including two with significant revenue potential, as customer confidence increased through the Revenue Durability Assessment™.

Innovation: Two emerging product innovation opportunities were identified that could strengthen the company’s competitive advantage.

Service Improvements: Six customer-recommended service improvements were identified.

Customer Relationships: The assessment strengthened customer relationships by engaging customers in strategic discussions about future needs.

Following the assessment, the leadership team established a 12-month Revenue Durability Score™ target of 7.9 to guide future improvement.

M&A Decision Signals

1. Demand Durability

View: Stable and improving

Demand is currently above sector baseline and structurally stable, supported by a modest-to-high level of perceived innovative value. The upward trajectory toward 7.9 suggests strengthening customer relevance and improving resilience of underlying demand, which should enhance buyer confidence in forward revenue projections.

Opportunity: Increasing demand stability supports stronger valuation confidence.

Risk: Demand durability remains below Innovator level (8.0+), limiting premium “certainty” pricing.

2. Growth Repeatability

View: Moderately strong with improving consistency

The score profile indicates that growth is increasingly repeatable rather than episodic, with improving retention and expansion dynamics implied by movement toward Growth Accelerator thresholds. This suggests a growing ability to reproduce revenue outcomes across periods and customer cohorts.

Opportunity: Greater predictability of recurring and expansion-driven growth.

Risk: Repeatability may still be sensitive to execution consistency and customer value delivery.

3. Revenue Quality

View: Above average and improving

At 7.3 versus a 7.0 sector average, revenue quality is better than peer norm, indicating healthier customer retention and more stable revenue composition. The trajectory toward 7.9 suggests continued improvement in the balance between acquisition and retention-driven revenue.

Opportunity: Higher proportion of durable, retention-led revenue supporting valuation resilience.

Risk: Revenue quality has not yet reached Innovator-level strength, limiting premium multiple expansion.

4. Revenue Visibility

View: Improving but not yet high-certainty

Revenue visibility is improving as the company moves toward higher durability thresholds, but remains below levels typically associated with Innovator (8.0+) or Game-Changer (8.5+) certainty. This indicates moderate forecasting confidence with strengthening forward predictability.

Opportunity: Improved forecast reliability supports better deal underwriting and valuation confidence.

Risk: Visibility may still fluctuate if customer behaviour or execution consistency weakens.

5. Customer Concentration Risk

View: Not elevated, but requires continued monitoring

While the data does not indicate acute concentration risk, the company is not yet at a level of maturity where diversification effects are maximised. As durability improves toward 7.9, concentration risk is expected to gradually reduce through broader and more stable revenue distribution.

Opportunity: Diversification likely to improve naturally with stronger expansion dynamics.

Risk: Any hidden dependency on key accounts could still materially impact durability perception in due diligence.

Overall M&A Interpretation

The company demonstrates above-sector and improving Customer & Revenue Strength, with a clear 12-month trajectory toward stronger durability, higher repeatability, and improved revenue quality. This supports increasing buyer confidence in forward revenue projections, while still reflecting a business that has not yet reached high-certainty Innovator-level predictability.

From an M&A perspective, the profile suggests a company moving toward more defensible, repeatable, and visible revenue streams, improving valuation robustness, while remaining sensitive to execution consistency and continued progress toward higher durability thresholds.

Revenue Quality & Buyer Confidence Improvements

Companies use their Revenue Durability scores as a structured basis for ongoing conversations with customers about the level of innovative value they expect the company to deliver in the future.

These conversations generate direct customer input on:

- where products and service delivery can be improved to reduce revenue risk,

- what current and emerging customer needs are,

- and where demand for innovation may create new growth opportunities.

This customer-level input is then processed and analysed within the platform to produce a company-specific view of growth prospects, revenue risk, and future value creation potential.