Will this borrower sustain and grow the revenue required to service debt?

Revenue Durability™

Capability to win, retain, and expand customers

Revenue Durability™ provides customer-validated evidence of how well a company is positioned to continue winning, retaining and expanding customers. It specifically reveals threats to existing revenue and expansion potential over the next 12 months, based on customers’ expectations of future value, innovation demand and emerging unmet needs, while also indicating broader customer-acquisition potential.

It is a repeatable predictive measure derived from customers’ ratings of the innovative value they expect a company to deliver in the future, measured on a scale of 1–10. These ratings indicate how effectively the company is adapting to customers’ evolving needs.

By weighting customer expectation scores by current revenue, the Revenue Durability Score estimates future revenue retention, growth potential within existing customers, and ongoing demand for innovation.

What the bank learns:

- Is customer demand sustainable?

- Is revenue concentration risk increasing?

- Are revenues likely to remain durable throughout the lending term?

Credit question answered: “How dependable is future revenue generation?”

Assessment Illustration

Bank Credit Summary — 12-Month Revenue Durability: Risks & Opportunities

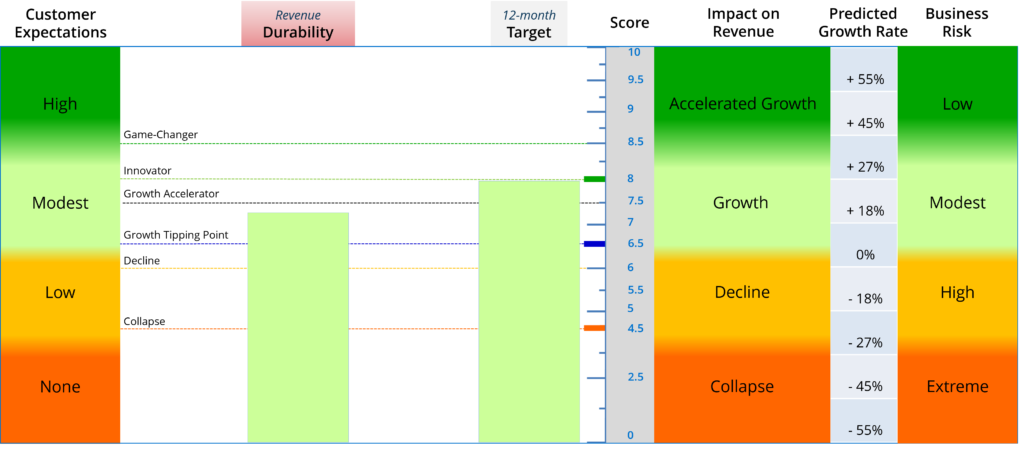

The company’s Customer & Revenue Durability score of 7.3 is above both the All Sector Average (7.0) and the Growth Tipping Point threshold (6.5), indicating a revenue profile that is currently resilient and trending positively. With a 12-month target of 7.9, the business is positioned to move from a solid durability profile toward the upper end of the Growth Accelerator range, supporting increased confidence in future revenue generation from a lending perspective.

Post-Assessment Opportunities

The Revenue Durability Assessment™ uncovered the customer-validated opportunities below through structured conversations about the innovative value customers expect the company to deliver in the future. This customer rating process builds trust, measures how well the company is adapting to evolving customer expectations, and creates a platform for strategic discussions that uncover new revenue and growth opportunities.

Sales: Five immediate sales opportunities were identified, including two with significant revenue potential, as customer confidence increased through the Revenue Durability Assessment™.

Innovation: Two emerging product innovation opportunities were identified that could strengthen the company’s competitive advantage.

Service Improvements: Six customer-recommended service improvements were identified.

Customer Relationships: The assessment strengthened customer relationships by engaging customers in strategic discussions about future needs.

Following the assessment, the leadership team established a 12-month Revenue Durability Score™ target of 7.9 to guide future improvement.

Bank Decision Signals

A: Credit Opportunities

Customer Demand Appears Sustainable

The current score suggests customer demand is supported by a modest-to-high expectation of innovative value, indicating that customers continue to perceive sufficient value to maintain engagement and purchasing behaviour. The trajectory toward 7.9 implies strengthening customer relevance and improving resilience of future demand.

Revenue Durability Is Strengthening

The company is already operating above sector norms and is expected to progress toward Growth Accelerator levels over the next 12 months. This suggests improving retention dynamics, greater revenue stability, and stronger support for predictable cash-flow generation during the lending period.

Improving Revenue Quality Supports Creditworthiness

The positive movement from 7.3 toward 7.9 indicates a business that is becoming increasingly capable of sustaining and expanding revenue from its existing customer base. This strengthens confidence that future revenues can support debt-servicing requirements and reduces the likelihood of revenue volatility.

Above-Average Position Relative to Peers

The company currently outperforms the sector average, providing evidence that its customer and revenue fundamentals are stronger than those of a typical peer business. This relative strength supports a more favourable credit outlook.

B: Credit Risks

Revenue Durability Has Not Yet Reached Innovator Levels

Although the trajectory is positive, the current score remains below the Innovator threshold (8.0). This means revenue resilience is improving but not yet at a level that would indicate exceptionally strong demand durability or very high predictability.

Customer Concentration Risk Cannot Be Fully Ruled Out

The durability score suggests a healthy revenue base, but concentration risk cannot be directly measured from this data alone. A lender should continue to assess customer concentration, contract exposure, and dependency on key accounts as part of broader credit diligence.

Execution Against the Improvement Target Is Required

The projected improvement from 7.3 to 7.9 is not automatic. Failure to continue strengthening customer value delivery, retention, and expansion dynamics could slow progress toward Growth Accelerator performance and reduce the expected improvement in revenue resilience.

Credit Interpretation

From a lending perspective, the company demonstrates above-average revenue durability with a positive forward trajectory, suggesting that future revenue generation is reasonably dependable. Customer demand appears sustainable, there is no indication that revenue concentration risk is increasing, and revenues are likely to remain durable throughout the next 12 months provided the current improvement trajectory is maintained.

Overall, the profile supports a view of moderate-to-strong credit quality, with opportunities arising from improving revenue resilience and customer value strength, balanced against the need to continue executing toward the targeted durability improvement.

Client Revenue Durability Improvements

Companies use their Revenue Durability scores as a structured basis for ongoing conversations with customers about the level of innovative value they expect the company to deliver in the future.

These conversations generate direct customer input on:

- where products and service delivery can be improved to reduce revenue risk,

- what current and emerging customer needs are,

- and where demand for innovation may create new growth opportunities.

This customer-level input is then processed and analysed within the platform to produce a company-specific view of growth prospects, revenue risk, and future value creation potential.